The expiration of enhanced premium tax credits at the end of 2025 has driven significant cost increases for Affordable Care Act Marketplace enrollees. A follow-up survey by the Kaiser Family Foundation reveals that half of returning participants now report substantially higher premiums and deductibles. This financial shift is altering coverage decisions and household spending patterns across the United States.

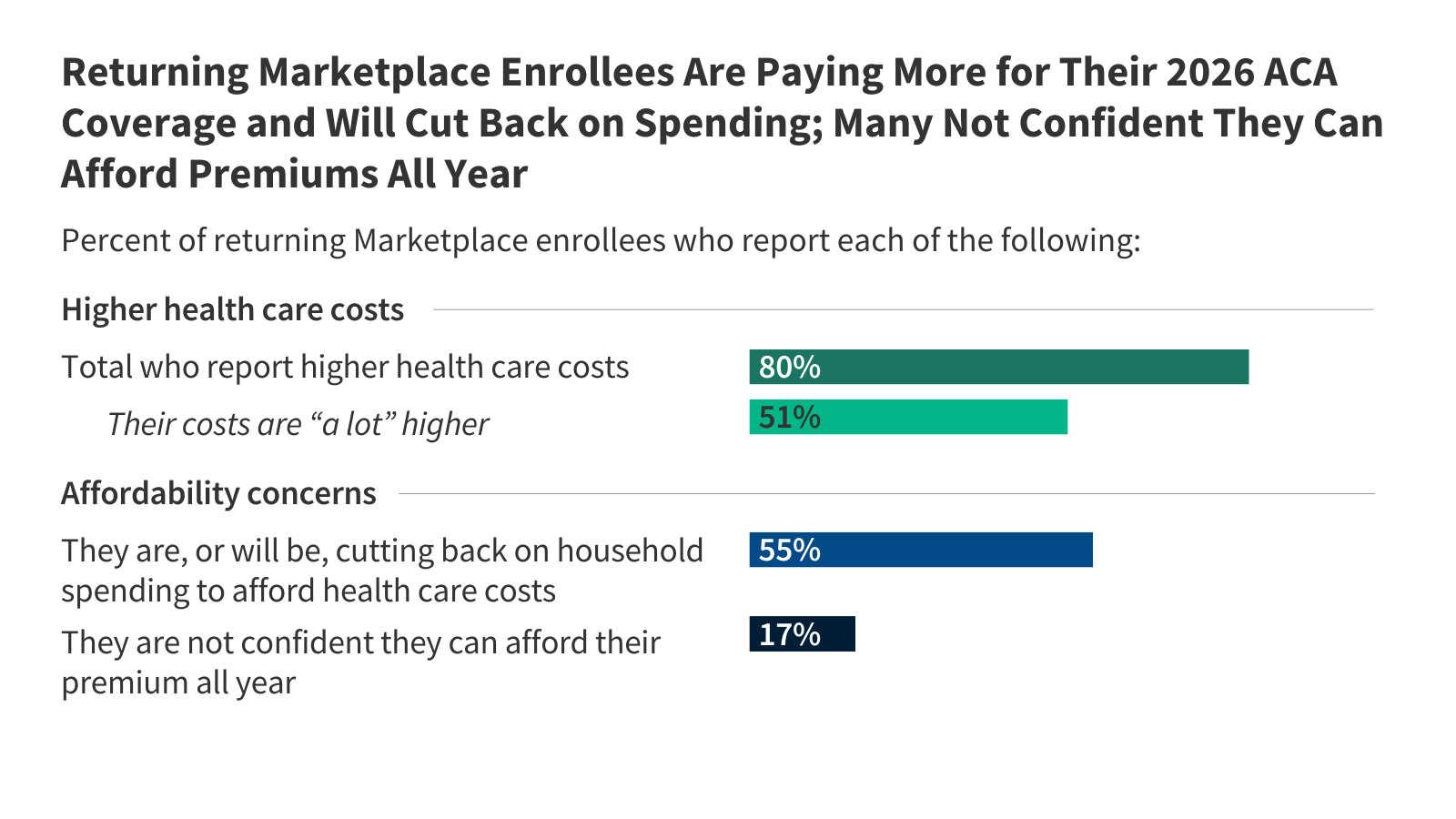

Eighty percent of individuals who re-enrolled in 2026 indicated that their out-of-pocket expenses or premiums rose compared to the previous year. Fifty-one percent described these increases as a lot higher, signaling a sharp departure from the subsidized stability of 2025. The data reflects the immediate impact of the policy change on consumer affordability.

Economic strain is forcing many families to prioritize medical coverage over basic necessities. Fifty-five percent of returning enrollees stated they are cutting back on food or household items to afford their insurance. This burden is even heavier for those with chronic conditions, where 62% report similar financial sacrifices. The situation highlights a trade-off between health security and basic survival needs in the current economic climate.

Coverage churn has accelerated as some individuals exit the marketplace entirely due to unaffordability. One in 10 (9%) of the original 2025 enrollees are currently uninsured, while three in 10 (28%) switched to different plans. Younger adults between ages 18 and 29 show the highest rate of departure, with nearly half leaving the system.

The risk pool dynamics present a significant challenge for market stability. Insurers anticipate this trend, as the departure of healthier, younger enrollees can destabilize the financial foundation of the system. The Kaiser Family Foundation noted that this exodus contributes to an enrollee base that is more expensive on average per capita. Such dynamics often lead to further premium hikes in subsequent years, creating a feedback loop of rising costs.

Financial concerns are shaping political behavior ahead of the 2026 midterm elections. Forty-eight percent of registered enrollees say health care costs will impact their voting decision. Democrats express significantly higher concern regarding this issue compared to Republicans.

Direct accounts from enrollees highlight the severity of the price jumps. A 34-year-old man in Texas noted that premiums for two people reached $800 per month without subsidies. Another participant in Florida reported premiums rising from $2000 to $3500 for a household of four. These personal stories illustrate the broader statistical trends regarding subsidy loss and affordability gaps.

The policy background involves the sunset of enhanced credits that were originally temporary. Without these credits, many households earning above certain thresholds lose eligibility for significant assistance. This structural change effectively shifts the cost burden directly to consumers.

Looking ahead, the risk of coverage loss remains high for those unable to pay monthly premiums. One in 6 (17%) of returning enrollees say they are not confident they will afford their insurance premiums for the entirety of 2026. Four percent of returning enrollees have not yet paid their first premium for the year. Grace periods exist but do not guarantee long-term retention without financial relief.

Market stability will depend heavily on legislative responses or consumer adaptation to the new cost reality. Stakeholders will monitor enrollment numbers closely as the 2026 open enrollment cycle concludes. The outcome could influence future health policy debates in Washington and reshape the economic landscape for millions. Analysts suggest the situation requires immediate attention to prevent long-term market fragmentation.