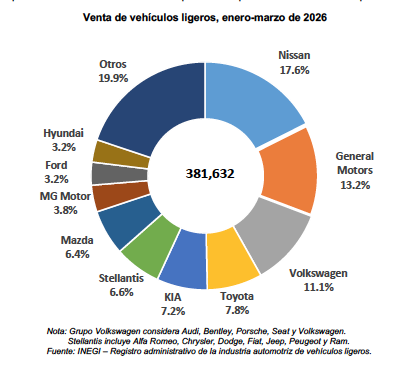

Mexico's automotive market reached a new milestone in the first quarter of 2026, with light vehicle sales exceeding 381,000 units. This performance breaks the previous record set in 2017, contrasting sharply with a visible slowdown in the United States.

Financial expert Manuel Herrejón Suárez notes that the US market is showing signs of cooling as American consumers become more cautious. He points to declining sales from major players like Ford as an early indicator of economic adjustment.

In Mexico, the surge in sales stems from aggressive supply strategies, particularly from Chinese brands, and a release of long-pent-up demand. This growth is occurring despite high interest rates and recent inflationary pressures.

Trade tensions and supply chains

Political shifts in the US are introducing new risks to the regional industry. Herrejón Suárez argues that the 'Trump effect'—the use of tariffs as a political and trade tool—is impacting investment expectations and supply chain configurations.

Because the North American automotive sector is highly integrated, trade friction directly alters production costs and logistics. Any shift in US trade policy toward Asia could force manufacturers to move production closer to the US border under USMCA rules.

While Mexico stands to benefit from nearshoring, Herrejón Suárez warns that the current domestic boom might not be structural. He suggests the Mexican market's reliance on low-cost imports and credit makes it vulnerable to external economic shifts.

Mexico remains a strategic assembly node rather than a full-value-chain producer. The country's long-term stability depends on its ability to transition into advanced manufacturing and strengthen local suppliers.